The past twenty-one months have been erratic to say the least.

Back in October, I wrote about the building industry’s Q3 economic performance and future outlook and how it was intertwined with COVID-19, supply chain issues, and labor shortages. At the time, there was uncertainty surrounding the delta variant and how it was influencing Q3 numbers.

Well, here we are in December, and there’s a new variant, omicron, plunging regions back into lockdown. That, combined with continued material and pricing woes are causing experts to speculate on how our currently fragile economic ecosystem will fare in the coming months and years.

The picture is cloudy, but I’ll look into my crystal ball and offer some potential outcomes and solutions. Before we get into that, let’s look at Q4 economic performance and some of the key indicators to keep an eye on.

Q4 Performance

Let’s start with the Architectural Billings Index (ABI).

The ABI is a measurement of architectural billings from month to month. A value greater than 50 means that architectural firms are reporting that they billed more this month than they did last month; a score of 50 means they billed the same; a score less than 50 signals a reduction in billings.

Generally, a score greater than 50 indicates that there is more design work occurring, which means more work for building firms down the pipeline.

See Figure 1 below. Billings scored over 50 in October and November, but the rate of billings has been decreasing throughout Q4. There was a tremendous growth in billings earlier this year, but that is leveling off, and the project pipeline is slowing down as a result.

Source: AIA.org

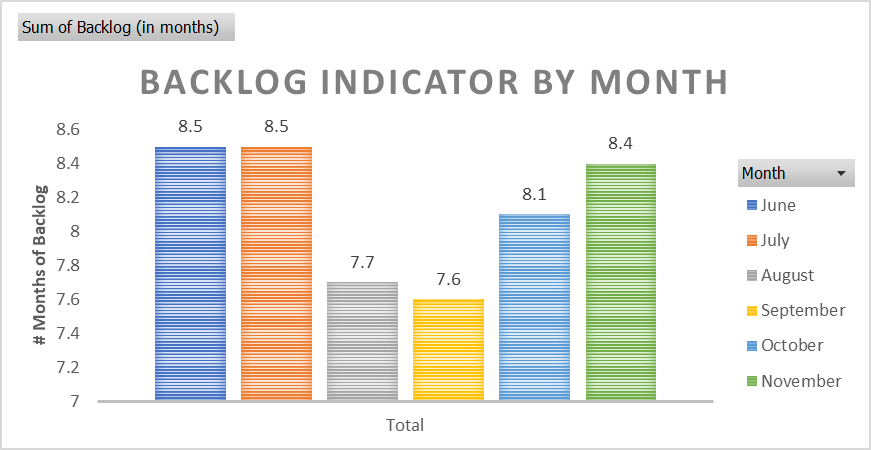

Aside from the ABI, The Associated Builders and Contractors’ (ABC) backlog indicator is another valuable source for monitoring building industry economic health. Backlog is a key performance indicator for every construction company; it measures the dollar amount of work that is under contract but is yet to be performed. ABC gathers this information by polling commercial construction contractors and converting their dollar value of backlog into number of months of expected work.

Figure 2 shows that backlog has moved in the opposite direction of the ABI over the last few months, i.e. while the ABI has been decreasing, backlog has increased. At first this may seem counterintuitive, but I believe this could be explained by the spike in ABI in August and September.

Think of it this way- new projects typically take a few months to move from design to construction, so naturally it will also take time for economic data to make its way from the ABI to contractor backlog.

Therefore, increased backlog is a positive indicator for contractors, but be vigilant considering that backlog could decrease in the next two months in the same way as the ABI.

Source: ABC.org

And one final thought on backlog:

It is often said that economic downturns hit the construction industry about nine months after they hit most other economic sectors; backlog is the reason for that. There is work still in the coffers when crisis strikes, but the problem is then securing work beyond that point. So any time we are looking at future outlook, sustaining backlog is one of the critical actions a construction firm needs to take to remain in good financial health.

To round out the Q4 performance, let’s take a look at inflation and the supply-chain.

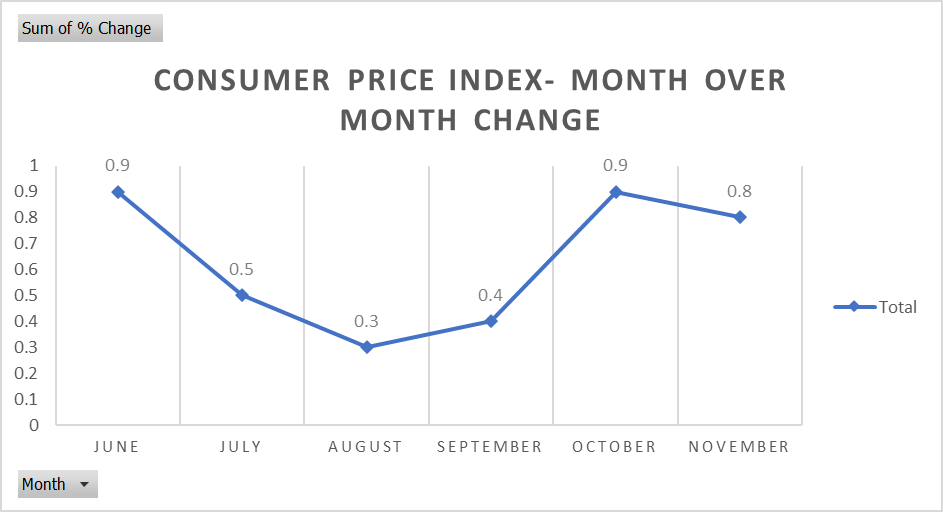

Figure 3 shows the consumer price index (CPI) over the past six months. The CPI measures the changes in price on goods from month to month. While Q3 saw rate increases slowing, Q4 has ramped back up. Compared to November 2020, the November 2021 CPI is up 6.8%, which is significant and one of the highest year over year increases since the 1970s. This means inflation has continued to run rampant.

Source: BLS.gov

This should not come as a surprise to building industry professionals. Material prices have continued to escalate and lead-times are still growing for common building materials. In short, supply and demand are in disequilibrium; there is more demand than the supply chain can handle. This must and will change.

Outlook: 2022 and Beyond

So where does that leave us for 2022? Well, the elephant in the room is COVID-19 and the omicron variant.

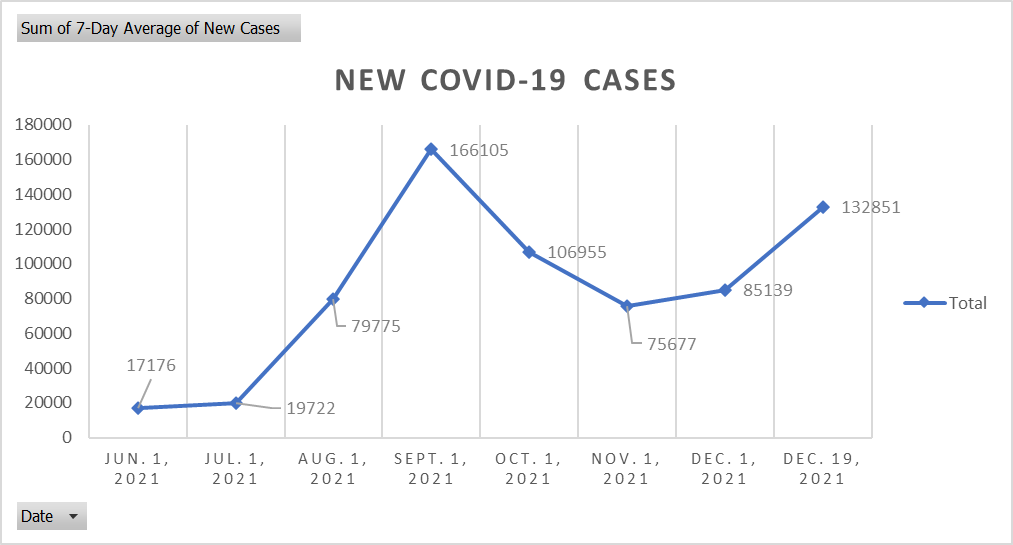

The omicron variant is relatively new to the COVID-19 landscape, with the World Health Organization (WHO) classifying it as a Variant of Concern on November 26, 2021. Figure 4 below illustrates the uptick in cases due to the delta variant (Aug./Sept.) and how that compares with the current rise in cases due to omicron in December alone.

Source: New York Times

Omicron is breaking through to many vaccinated people, so the upward trend in cases is going to continue and very well could look similar to early in the pandemic. The hope is that we are much more prepared to handle an outbreak this time around and that our businesses will fare better as a result.

While this will have to be true, the continued cyclical nature of variants emerging and de-railing economic progress should be concerning. The Fed cannot continue to give stimulus in the same way that it has over the past twenty-one months due to the threat of raising inflation further. As a result, Fed leadership has already made plans to slow bond purchases and raise interest rates in 2022. Bond purchases will begin to reduce as early as March 2022, and interest rates are speculated to increase to 0.9% at the end of 2022 and 1.6% at the end of 2023. Meanwhile, inflation is going to continue to be a problem in 2022.

In summary, there is a cause and effect to every action.

In this case, inflation is causing interest rates to increase with the eventual effect that capital (money) will not be as cheap for builders and developers to borrow in 2022 as it has been since the start of the pandemic. This increase in cost of capital will slow the rise of new projects, which leads to less backlog, which leads to tighter margins and more competition.

Therefore, securing backlog needs to be of top priority for the typical construction company in the current economic landscape. Backlog can get you through challenging times and may be the best solution for surviving any economic fallout associated with the pandemic.

At this point, you should be asking yourself: “What am I doing to secure more backlog?”

Owners and leaders should be looking to projects taking place in 2022, 2023, and beyond for that answer. Don’t just settle for the jobs that start next month. Sell your clients on the concept of securing long-term work where you can team up as partners (potentially in a design-assist capacity) early and guarantee long-term stability. In return, your clients receive a dedicated teammate who will be better suited to execute the project by having a deeper understanding of the stakeholders and their needs.

Even with that said, not everything is bleak about the future.

There will be new projects as a result of the Infrastructure Bill as well as plenty of developers who recognize that even if capital is more expensive in 2022, it is still cheaper than it has been during many economic downturns of the past.

The fact that backlog is up means that contractor confidence is up. View that confidence with a cautious optimism because we can speculate all we want about the future, but nothing is certain. So control what you can control, and go out and secure work for 2022 and 2023 right now.

Authored by:

Matt Verderamo

19 December 2021

email me! mverderamo@allianceexterior.com