In last week’s edition of Talking Shop, I explored the current state of the global economy and supply chain, and how it will affect the building industry in the coming months and years. I looked at low interest rates, extended lead times on common construction materials, and the problem with demand exceeding supply.

Recap: Inflation is up, raw material pricing is up, uncertainty is up!

On Wednesday, September 29th, the Associated Builders and Contractors (ABC) hosted a Q3 Economic Update & Forecast with their Chief Economist, Anirban Basu. For those that don’t know Anirban Basu (this was my first exposure to him), he was fantastic. The presentation was insightful, but also fun and engaging. I followed him on LinkedIn shortly after and look forward to learning more from him the future. After listening to him, it only seemed right to build on last week’s post and spend this week breaking down some of the key takeaways from that presentation for the Talking Shop readers. So, without further ado…

The Facts:

Aside from inflation and other economic factors, filling JOBS continues to be one of the biggest problems for our industry. Quick hits:

- August’s jobs report was disappointing for the economy as a whole; only 235,000 jobs were added compared to the 720,000 that were forecasted. This slowdown is being attributed to the uncertainty surrounding the Delta variant.

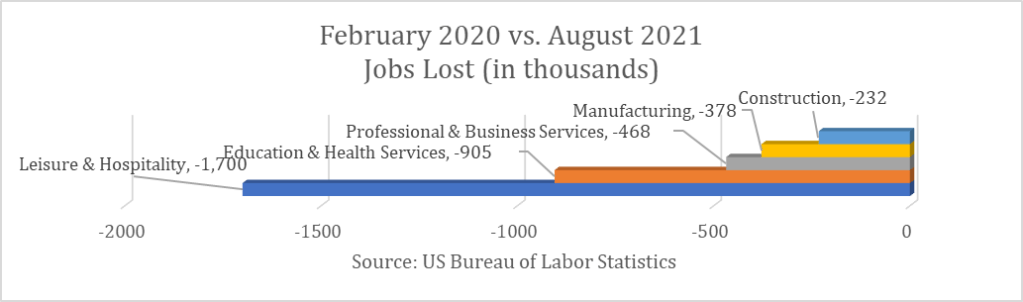

- Since February 2020, the construction industry has lost 232,000 jobs. According to a U.S. Bureau of Labor Statistics report from March 2021, the construction industry needed to hire 430,000 workers in 2021 to meet demand. This has obviously been going in the wrong direction, and despite it being a topic of discussion for quite some time, the skilled labor shortage continues to be a cause for concern.

- Figure 1 shows a few of the other sectors losing the most jobs between February 2020 and August 2021:

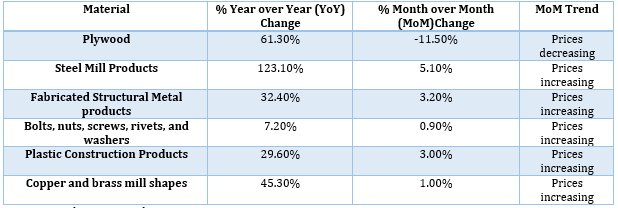

I touched on it last week, but INFLATION continues to be a topic of concern. The US Bureau of Labor Statistics quantifies inflation through their Producer Price Index (PPI). Below are a few materials and how they have been trending over the last few month.

Source: US Bureau of Labor Statistics

Lastly, the ARCHITECTURAL BILLINGS INDEX (ABI) spent March 2020 through January 2021 below 50 (indicating that billings have decreased), however it has remained above 50 since February of this year, with a score of 54.6 in July.

The Takeaways:

Starting with the JOBS section.. Figure 1 shows the number of jobs lost in a few key industries. It is interesting to consider how the loss of jobs in each industry will eventually translate into the loss of building projects in those industries. Leisure & Hospitality is a good example- the industry was hit hard by the peak of the lockdowns, and travel and tourism continue to be inconsistent. It is going to take months for hotel occupancy to rise and call for more hotel construction. On the other hand, Education & Health Services is a less obvious member of the list. My personal experience through the last eighteen months has been that the higher education and health care industries are still building at a strong rate. This could be attributed to those projects having a higher backlog prior to the pandemic, but I believe that there is a need for quality institutional and health care buildings. I’m hopeful that will continue. And lastly, the decrease in manufacturing jobs is another indicator of why the building industry is having trouble finding adequate supply for the demand. It is imperative that manufacturing facilities get back to full operational capacity.

INFLATION is tied to the jobs report as well. The Federal Reserve is watching the jobs reports closely to determine when the economy reaches near-full capacity so it can begin to raise interest rates. Until that happens, demand and supply will continue to be in disequilibrium and cause higher prices and a more volatile supply chain.

And finally, the uptick in the ARCHITECTURAL BILLINGS INDEX (ABI) is a positive sign for the building industry because it means there is more design activity. The question remains, will more design activity translate into more building activity? Many contractor connections I have spoken to have mentioned they are doing more and more budgeting and “repositioning” pricing exercises over the last few months. This means there are projects in design, but the projects are not making that crucial transition into construction documents and eventually construction. Apartment complexes are the outlier in this trend as developers are continuing to build; rent pricing continues to increase, and higher rents justify new construction. Again, the question is how long will this last? It will not be forever, so this will be an especially interesting market to track over the coming months.

In summary, demand and supply will reach equilibrium, but there will be some challenging times ahead for the building industry. ABC’s Q3 economic update painted a picture of the economic landscape we are living through, and I hope this post makes it digestible for you as the reader. Use this as your cheat sheet for your next call with a client! The goal is to present you all with relevant, insightful, and far-reaching knowledge.

Thanks for reading, and Happy Wednesday.

Authored by:

Matt Verderamo

5 October 2021

Works cited:

Construction industry needs to HIRE 430,000 workers this year SAYS ABC. (n.d.). Retrieved March 27, 2021, from https://www.constructionbusinessowner.com/news/construction-industry-needs-hire-430000-workers-year-says-abc

One thought on “#3- Q3 Economic Recap & More Outlook”